Understanding Technological Revolutions: A Framework for the AI Cycle

Carlotta Perez: Technological Revolutions and Financial Capital

A few weekends ago I sat down to re-read Carlota Perez’s book Technological Revolutions and Financial Capital. It’s a book I’d worked through once before, three or four years ago, and one I had filed away as interesting but not particularly urgent. Re-reading it in May 2026, alongside the Coatue deck I covered last week and the Q1 2026 software earnings I covered before that, my view of it has changed considerably. It is now, in my opinion, one of the most useful single frameworks I have for thinking about where we sit in the current AI cycle — and the fact that it was written in 2002, before AI, before the smartphone, before the post-crisis recovery, before any of this, makes that doubly striking.

For those who haven’t come across her, Perez is a Venezuelan-British researcher who has spent forty years studying the long-arc relationship between technological revolutions and the financial, institutional, and political systems they sit inside. Technological Revolutions and Financial Capital is her central book. It is the source — usually uncredited — of a lot of the vocabulary now floating around investor research notes: “installation phase,” “frenzy,” “deployment,” “turning point,” “techno-economic paradigm.” Coatue’s six-phase cycle framework that I worked through last week is built directly on her foundations.

In this piece I want to do three things. First, walk through Perez’s core framework properly. Second, work through the specific concepts that make her model distinctive: the cheap input that anchors each paradigm, the four sub-phases within every surge, the decoupling of financial from production capital, the role of institutions, and the shift in “common sense” that each revolution forces. And third, overlay all of this against where we sit in the AI cycle today and where we’re potentially heading. As always, this is my attempt to take a complex, multi-layered set of dynamics and distil them into something useful for readers.

1. Who Is Carlota Perez, and Why Does the Book Matter?

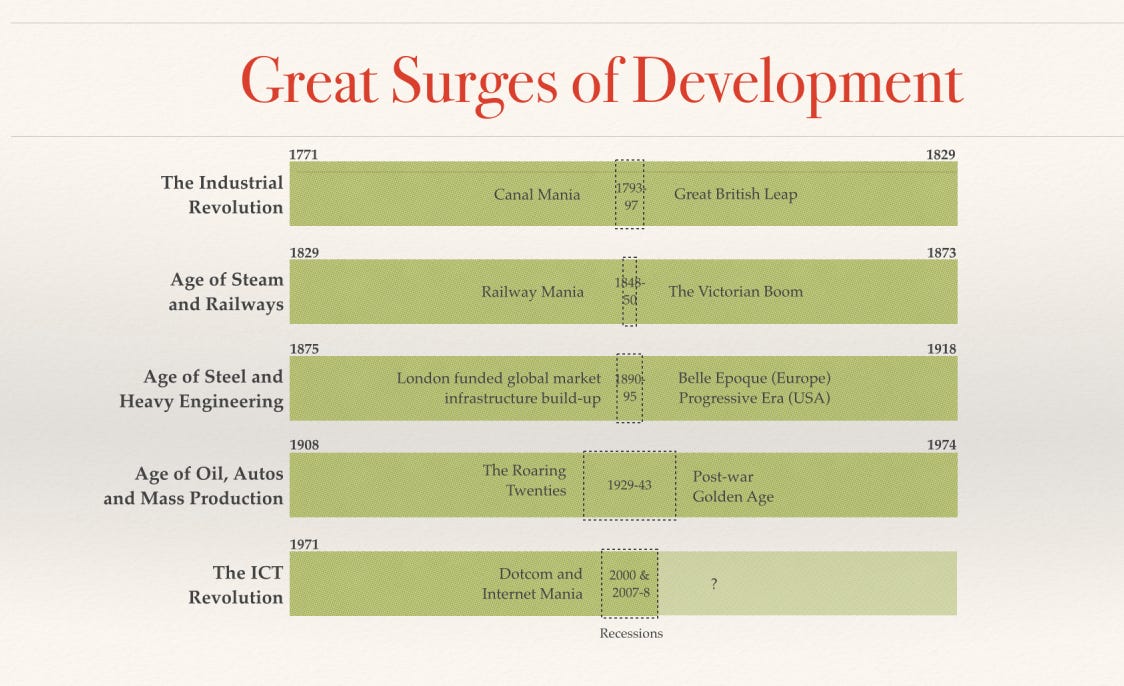

Carlota Perez has spent her career working on the long-arc question of how technological change interacts with financial markets, institutional structures, and political economy. She trained as an economist, worked across academia and government in Latin America, and is now one of the most-cited voices in the literature on long technology cycles. Her central claim — first set out in Technological Revolutions and Financial Capital in 2002 — is that the relationship between technological change and economic transformation is not random. It follows a remarkably consistent pattern, repeated five times across the last 250 years, and arguably visible now in the sixth surge currently underway.

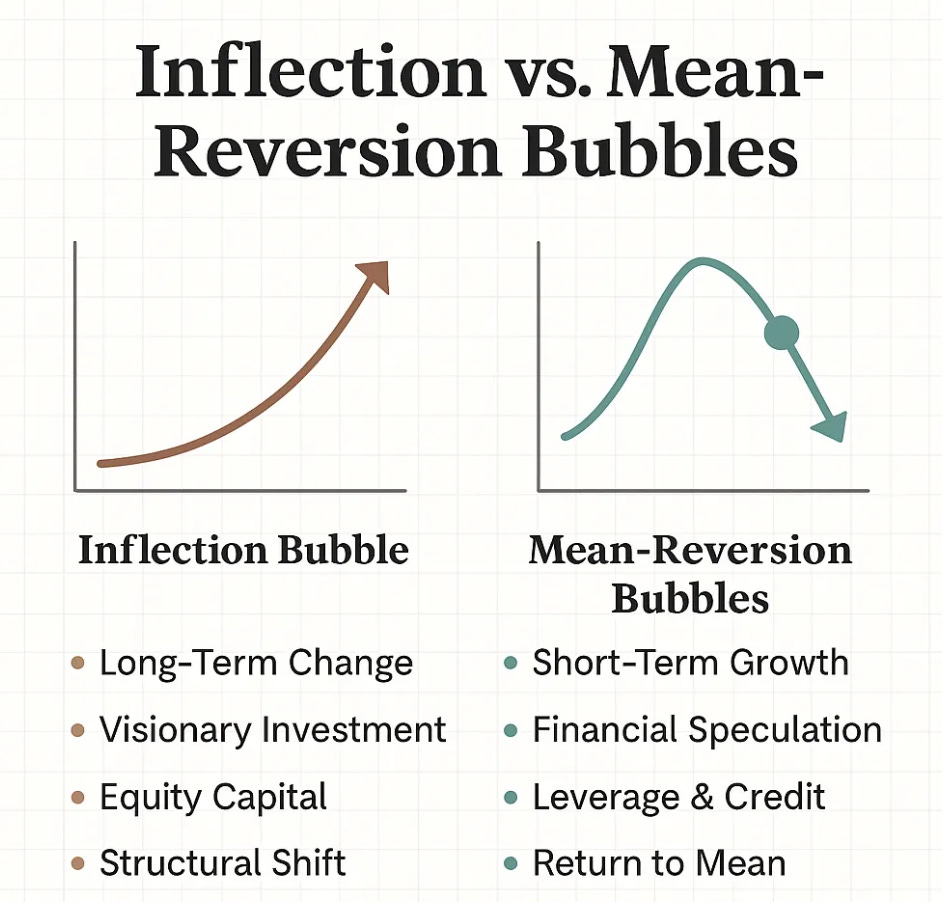

The book’s argument rests on three propositions. The first is that economic history since the Industrial Revolution has been organised around five great surges of development, each lasting roughly 50–60 years, each anchored in a cluster of innovations — what Perez calls a “techno-economic paradigm” — that reshape not just the products on the market but the underlying logic of how economic activity is organised. The second is that each of these surges follows the same internal structure: an initial installation period driven by financial capital and culminating in a bubble; a turning-point crisis; and then a deployment phase, where productive capital takes over, the technology diffuses through the broader economy, and the productivity gains are widely realised. The third — and this is the proposition that most distinguishes Perez from earlier theorists of innovation like Schumpeter or Kondratiev — is that the bubble is not a flaw of the system. It is part of the mechanism. Financial capital's willingness to over-invest is what builds the infrastructure that the deployment phase later uses. This is something I've written about at length, comparing 'inflection-related' bubbles to 'mean-reverting' ones — not all bubbles are the same, and some are structurally necessary (such as the one we're in today).

What makes the book genuinely useful, as opposed to merely academic, is that Perez is not making a deterministic claim. She is not arguing that the cycles are identical in length, or that the outcomes are pre-determined. What she is arguing is that the structure repeats, even if the details vary, because the structure is rooted in the underlying mechanics of how financial markets, institutions, and societies respond to disruptive technologies. Financial capital chases novelty. Institutions lag innovation by decades. And the gap between the two is what creates both the bubbles and the eventual crises. Embedded in this is a concept she keeps returning to throughout the book — the idea that each new paradigm requires not just new technology but a new common sense. New mental models about what counts as a good business, a sensible career, a defensible moat, a worthwhile investment. The paradigm shifts the operating logic of the economy at the same time it shifts the technological frontier.

For investors, the practical value of the framework is that it gives you a map. If you can locate where you sit in the surge, you can position accordingly. Frenzy-phase positioning looks very different from synergy-phase positioning, and the most common mistake — repeated in every cycle — is to extrapolate frenzy-phase winners into the deployment phase. The companies that lead during installation are rarely the same companies that lead during deployment.

The book has aged unusually well. Perez wrote it in the immediate aftermath of the dot-com crash, which she correctly identified, in real time, as the frenzy peak of the fifth surge. She predicted, accurately, that a turning-point crisis would follow within roughly a decade. She underestimated, in my view, how long the deployment phase of the ICT surge would take to mature, and she did not anticipate that AI would emerge as the technological core of a new surge rather than as a continuation of the existing one. But the framework holds, and the concepts she developed two decades ago are fundamentally useful tools for reading what’s happening now.

2. The Five ‘Surges’ of a Technological Revolution

Perez identifies five great surges of development since the Industrial Revolution. Each is anchored in a “big bang” — a single moment of innovation that marks the beginning of a new techno-economic paradigm. Each lasts roughly 50–60 years from big bang to maturity. And each transforms not just the industries directly involved but the entire organising logic of the economy around them.

The unifying mechanic across all five surges is what Perez calls the key factor, or the “cheap input.” Every surge is anchored around a particular resource or input that becomes structurally cheap and pervasively abundant at the start of the paradigm. The economics of the cheap input is what makes the new techno-economic logic possible. Once the input falls in price to the point that it can be used recklessly, used everywhere, used as the default building block for everything, the surge becomes economically viable. Cotton was that input for the first surge. Coal was that input for the second. Steel and electricity for the third. Oil for the fourth. Cheap microelectronics — Moore's Law — for the fifth. The commoditisation of intelligence — Jevons paradox — is the current one.

Working through the five Perez surges with that lens:

The first surge starts in 1771, with the opening of Richard Arkwright’s mill in Cromford. The technological core is mechanisation, water power, and the early factory system. The cheap input is cotton and mechanical power. The financial frenzy is the canal mania of the 1790s, which built the transport infrastructure for industrial output. The bubble bursts. The turning-point crisis follows. The deployment phase sees the mechanised cotton industry diffuse across Britain, Europe, and eventually the world.

The second surge starts in 1829, with the test of Robert Stephenson’s Rocket on the Liverpool–Manchester railway. The technological core is steam, coal, and rail. The cheap input is coal-powered motive force. The financial frenzy is the railway mania of the 1840s — speculative capital flowing into thousands of miles of rail track, much of it never economic on its own terms, but ultimately leaving behind a transport infrastructure that the deployment phase used to build the Victorian industrial economy.

The third surge starts in 1875, with the Bessemer steel plant at Carnegie’s Edgar Thomson Works. The technological core is steel, electricity, and heavy engineering. The cheap input is cheap steel and electric power. The bubble runs through the late 1880s into the early 1890s, with railroad over-extension and the 1893 panic acting as the turning-point crisis. Deployment delivers the Belle Époque industrial expansion.

The fourth surge starts in 1908, with the Model T rolling off the line at Ford’s Highland Park plant. The technological core is oil, the automobile, and mass production. The cheap input is cheap oil and the internal combustion engine. The financial frenzy is the late 1920s. The turning-point crisis is the 1929 crash and the Great Depression. The deployment phase — interrupted but not stopped by the Second World War — is the post-war boom of mass production, mass consumption, and the suburban middle class. This is what Perez refers to throughout the book as the Golden Age.

The fifth surge starts in 1971, with the launch of the Intel 4004 microprocessor. The technological core is information and telecommunications. The cheap input is microelectronics — Moore’s Law made compute essentially free at the margin. The financial frenzy is the dot-com bubble of the late 1990s. The turning-point crisis runs, in Perez’s reading, from the 2000 crash through the 2008 financial crisis. The deployment phase has been unfolding since — internet, smartphones, cloud computing, e-commerce, mobile-everything.

The sixth surge — and this is my own extension of the framework, not Perez’s — appears to have started in 2020–2022, with the launch of GPT-3 followed by ChatGPT. The technological core is foundation models, agentic systems, and autonomous workflows. The cheap input, structurally, is intelligence. The same way Moore’s Law made compute almost free, AI is making cognitive work increasingly close to free. That is the underlying economic shift driving the token-volume curve, the payroll-anchored TAM, and the application-layer monetisation thesis I’ve been writing about. It is the same dynamic Perez describes in the previous five surges, dressed in new technology.

What is most striking about the historical pattern, when you lay the surges out side by side, is the consistency of duration. Each runs roughly 50–60 years from big bang to maturity. Each has a financial frenzy that peaks roughly 25–30 years in. Each has a turning-point crisis that follows within a few years of the frenzy peak. And each deployment phase lasts another 25–30 years. The cycles are not identical, but the structure is robust enough that an investor who understood the pattern could have positioned themselves correctly across any one of them.

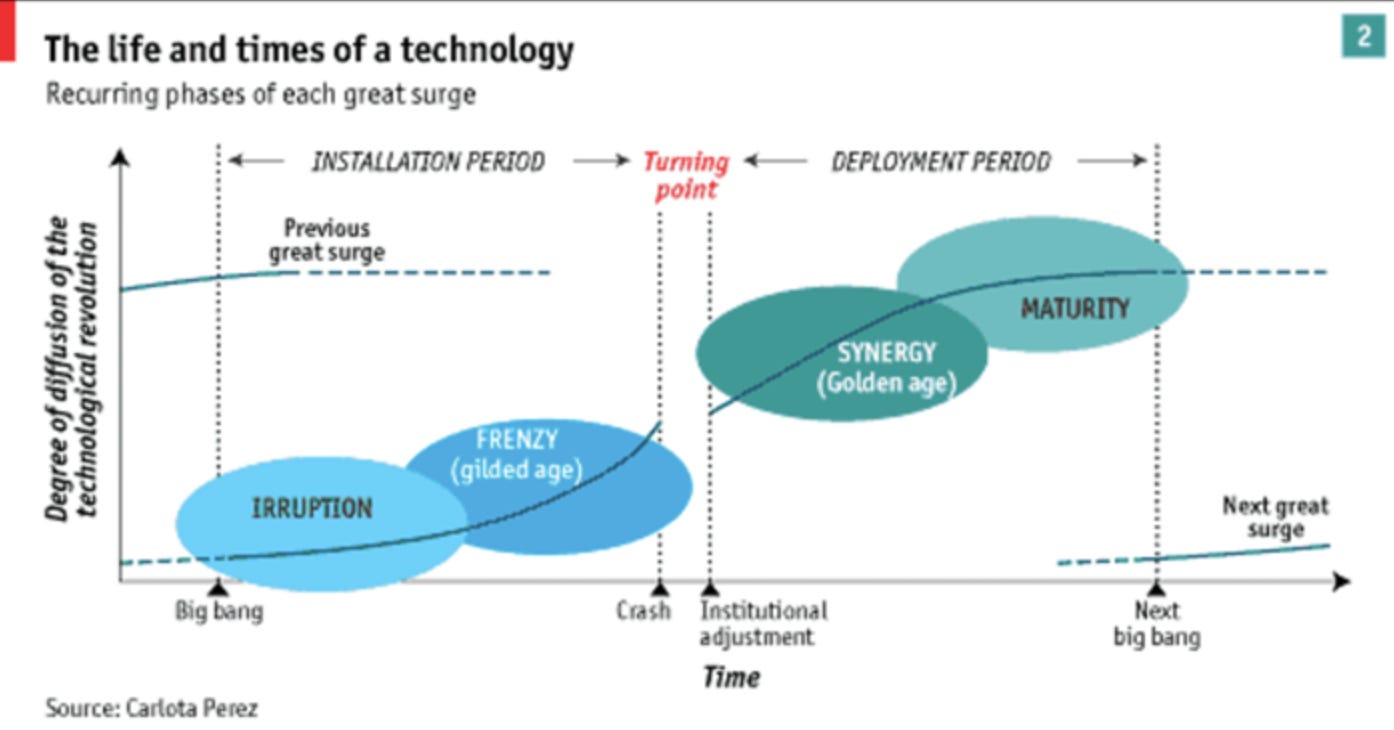

3. Installation vs Deployment — The Four Phases of Every Surge

A core principle in Perez’s book is the distinction between the installation period and the deployment period of each technological surge.

The installation period is the first half of the surge — the years during which the new technology is being built into the economy. Infrastructure is being constructed. Capital is flowing in to lay the groundwork. The new paradigm has arrived but hasn’t yet replaced the old one as the operating logic of the broader economy. Financial capital is in command during installation, because the long-term implications of the technology are uncertain enough that rational production capital won’t yet underwrite it. The speculative end of the market takes the lead, and over-investment is the norm rather than the exception.

The deployment period is the second half — the years during which the technology actually gets used at scale across the broader economy. The infrastructure built during installation gets productively utilised. The new paradigm becomes the dominant operating logic, replacing the previous one. Productivity gains diffuse from the innovating sector outwards. Production capital takes over from financial capital, and the speculative dynamics calm down. The deployment phase is when most of the actual economic value of a technological surge gets created — the bulk of the productivity gains, the broad-based prosperity, the institutional reorganisation around the new paradigm.

They are not two halves of the same process. They are two structurally different periods, with different dynamics, different winners, different financial logic, and different relationships between technology and the rest of the economy. Within these two periods, Perez identifies four specific sub-phases:

Irruption — the early years after the big bang. The new technology arrives, early adopters scale, financial capital starts paying attention. Productivity gains are concentrated in the new sector. The broader economy is still operating on the previous paradigm. This is the “displacement” phase in the language of more recent cycle frameworks.

Frenzy — financial capital takes over completely. Speculation runs ahead of productive economics. Asset prices decouple from underlying earnings. Infrastructure is over-built relative to short-term demand. Income inequality rises sharply. The bubble inflates.

Synergy — the deployment period begins. After the turning-point crisis, production capital re-engages. Financial speculation calms. The infrastructure built during the frenzy gets productively utilised. Productivity gains diffuse across the broader economy. The technology becomes embedded in everyday workflows, supply chains, institutional structures.

Maturity — the technology saturates. Returns to incremental investment diminish. The paradigm reaches its productive limits. New innovations begin gestating that will eventually become the big bang of the next surge.

Installation is Irruption plus Frenzy. Deployment is Synergy plus Maturity. The turning-point crisis sits between them. And the dynamics on either side of that crisis are almost mirror images of each other.

The defining feature of installation is that financial capital is in command. The new technology is exciting, the long-term implications are uncertain, the path to mass commercial adoption is unclear. So the market does what the market does in those circumstances — it speculates. Financial capital pours into the new sector, and over time it begins to decouple from the real economy. During frenzy, asset prices and the productive economy detach. The signals that financial markets are sending — “this technology is worth almost anything” — stop bearing any relationship to the signals that the productive economy is sending — “we cannot actually absorb this much infrastructure productively yet.” The gap widens until it cannot widen any further. Then the bubble bursts.

After the crisis, the recoupling begins. Production capital re-engages. The infrastructure that was over-built during installation finally finds productive use. Asset prices and the real economy start sending each other consistent signals again. The deployment phase is, structurally, the recoupling phase.

The other dynamic Perez identifies is institutional inertia. Institutions are designed for the previous paradigm. Tax codes, labour laws, regulatory frameworks, capital allocation norms, education systems, even corporate governance structures — all of these are built around the operating logic of the surge that is now ending. When a new paradigm arrives, the institutions don’t adapt automatically. They lag, often by decades. And that lag is part of why the turning-point crisis happens. The crisis is not just a financial event; it is the moment when the friction between the new paradigm and the old institutions becomes unbearable, and the institutional framework is forced to adapt.

Two things matter enormously about this whole architecture. First, the companies that lead the installation period are usually not the same as the companies that lead the deployment period. The frenzy-phase winners — the canal companies, the railway promoters, the radio manufacturers of the 1920s, the dot-com darlings of the 1990s — frequently get crushed in the turning-point crisis. The deployment-phase winners are the companies that absorb the infrastructure left behind by the frenzy and use it productively. Carnegie Steel didn’t lead the railway mania; it benefited from the steel demand that railway expansion created. Amazon and Google didn’t lead the dot-com bubble; they emerged afterwards and built on the fibre optic and server infrastructure the bubble left behind.

Second, the political and institutional response is fundamentally different between the two phases. Installation typically corresponds with rising income inequality, rapid capital accumulation at the top, and growing political tension. Deployment typically corresponds with widening prosperity, institutional reform, and a longer period of social stability. The famous “regulatory adjustment” that follows every major financial crisis is not coincidental — it is part of how the system transitions from installation to deployment. The 1930s saw Glass-Steagall, the New Deal, and the post-war Bretton Woods system. The 2008 crisis saw Dodd-Frank, central bank reform, and an extended period of low rates that ultimately enabled the next surge to fund itself.

4. The Role of Financial Capital — Why Bubbles Are Part of the System

The most controversial — and in my view the most useful — argument in the book is that financial bubbles are not a failure of the system. They are a feature of it. They serve a specific function during the installation period of a technological surge: they fund the over-investment that builds the infrastructure that the deployment phase then uses.

This is not a popular view. Bubbles are typically discussed as if they are aberrations — irrational episodes, speculative manias, periods of collective madness that destroy value and disrupt the orderly progress of economic development. Perez’s argument inverts this. She points out that without the speculative over-investment of the railway mania, Britain would not have had the rail network that powered the Victorian industrial expansion. Without the canal mania, the Industrial Revolution’s logistics infrastructure would not have existed. Without the dot-com bubble’s $1 trillion of investment in fibre optic cable, server infrastructure, and software talent, the post-2002 internet would not have had the substrate it needed to scale.

Financial capital, in her framework, is necessary precisely because it is willing to over-invest. Production capital is rational; it invests against measurable returns. But the early stages of a new techno-economic paradigm are characterised by uncertainty so deep that rational investment cannot justify the infrastructure required. The economy needs irrational over-investment to build the substrate that the rational deployment phase will later use. The bubble is the mechanism by which that over-investment is mobilised. It is also the mechanism by which financial capital decouples from the real economy — and the crisis is what forces the recoupling.

This does not mean every bubble is productive. Perez distinguishes between bubbles that build infrastructure (the railway mania, the dot-com bubble) and bubbles that destroy capital without leaving anything behind (Tulip Mania, certain commodity speculations). The productive bubbles are the ones tied to a genuine technological revolution; the unproductive ones are not. But within the structure of a technological surge, the bubble is doing real work, even if the individual investors who participate in it lose money along the way.

The implication for the present cycle is unsettling, but I think correct. If the current AI buildout is the installation phase of a new surge — and increasingly I think it is — then a bubble is not just possible but necessary. The $700B+ of hyperscaler capex, the Coatue-projected $12 trillion of cumulative AI infrastructure investment over 2026–2031, the over-investment in data centres, the geopolitical race for compute capacity, the speculative cheques being written into agentic startups — all of this is exactly the kind of over-investment that Perez’s framework predicts, and that the deployment phase will eventually use. The companies that participate may not all survive. The infrastructure they leave behind will be used by everyone.

This is why I have been pushing back, throughout my articles, against the simple “bubble = bad” framing. The current situation is uncomfortable. Valuations are extended. Capex is at historic highs. The political economy is tense. But the structural function of what is happening is to build the substrate for an extended deployment phase. The mistake is not to participate in the buildout. The mistake is to misjudge which companies survive the eventual turning-point crisis and lead the deployment phase that follows.

5. Where We Sit — Reading the Current AI Cycle

If Perez’s framework is right, the most important question for any investor right now is: where in the surge are we? The honest answer, in my view, is that we are in the middle of the installation period, somewhere between irruption and frenzy peak. We are not yet at the turning-point crisis. We are not yet in deployment. And the markers around us — the dispersion in public markets, the capex commitments, the hyper-exponential token growth, the talent flows, the policy debates — are textbook installation-phase behaviour.

A few specific anchors for where I think we sit.

The big bang for the current AI surge is the launch of GPT-3 in mid-2020, followed by ChatGPT in November 2022. ChatGPT is the moment when the broader market understood that a new techno-economic paradigm had arrived. That places us roughly four years into the irruption phase, which historically runs for 5–10 years before transitioning into frenzy.

The frenzy has not yet peaked. The clearest indicator is the dispersion regime I wrote about in the Coatue piece — the 85% spread between top-quintile and bottom-quintile public companies is now wider than at any point since 2009, and the speculation around frontier models, agentic startups, and AI-adjacent infrastructure is intensifying, not calming. Coatue’s six-phase framework — Displacement → Boom → Euphoria → Profit-Taking → Panic → Crash — places us in phase one. I have argued before that I think we are at the late end of displacement, transitioning into boom. We are not yet euphoric.

The financial capital signature is unmistakable. The $700B+ hyperscaler capex commitment for 2026, the $12T cumulative funding picture for 2026–2031, the OpenAI and Anthropic combined ARR running past $55B — faster than any prior software category in history — all of this is financial capital pouring into the new paradigm at a rate that classical production-capital logic cannot justify. The decoupling Perez describes — where asset prices and the productive economy detach — is becoming visible. Public AI valuations are not yet at dot-com peak distortion, but the gap between what financial markets are signalling about AI and what the productive economy can yet absorb is widening rapidly. That gap is the frenzy signature.

The shortage economy — the sellers of the shortage compounding margin while the buyers fund the build — is the financial capital signature played out in cohort terms. The 107% YTD return for shortage sellers (Nvidia, Broadcom, Micron, SK Hynix, the rest of the silicon, memory, and optical stack) against the 4% return for the capex-spending hyperscalers carrying the build cost on their balance sheets is a clean illustration of how financial markets reward the frenzy-phase winners while the deployment-phase winners are still building. The cohort spread is itself one of the more reliable signals of which phase of the cycle you are in. It widens through irruption, peaks in frenzy, and compresses once supply catches up with demand and the deployment-phase economics begin to look more attractive than the shortage trade. At current levels, the spread is at multi-decade extremes — consistent with mid-to-late frenzy rather than early irruption, and likely to compress meaningfully once the turning-point crisis arrives.

The common sense shift is also happening in real time. Perez argues that every paradigm forces a re-write of the operating logic of the economy — what counts as a good business, what counts as a sensible career, what counts as a defensible moat. The cloud-SaaS common sense of 2015–2022 (per-seat pricing, vertical SaaS, recurring revenue, "every company is a software company") is being actively replaced. The new common sense — agentic execution, outcome-based pricing, Service-as-Software, payroll-anchored TAMs, data flywheels as the durable moat — is what I have been writing about for the past year. You can see it in earnings calls, where public software companies are migrating from per-seat to consumption pricing. You can see it in venture deal memos, where the questions being asked of AI-native companies have fundamentally changed from twelve months ago. You can see it in M&A activity, in workforce reorganisations, and in the vocabulary that has shifted across the entire knowledge economy. The common sense is being rewritten in front of us.

The labour displacement debate is textbook installation-phase behaviour. Perez points out that income inequality typically widens during installation, that political tension around the technology rises, and that the institutional response lags by years or even decades. We are seeing exactly that. The $4T+ digital-AI TAM, anchored against global payroll, is the quantitative version of what Perez describes qualitatively in the book. I wrote about this in From SaaS to Service-as-Software — software is now competing for payroll budget, not IT budget, and the political economy implications of that shift are going to be considerable.

What we have not yet seen is the turning-point crisis. There has been no major correction in AI valuations. There has been no policy intervention that meaningfully alters the trajectory of the buildout. There has been no broad-based labour-market disruption that has forced institutional reform. All of these are predicted by the framework, and none have happened yet. Equally importantly, the demand signals themselves are still accelerating. Compute demand continues to grow exponentially — token volumes across the major API providers are compounding at roughly 12x year-on-year. GPU utilisation across the hyperscaler fleets is reportedly running at or near 100%, with Sundar Pichai publicly stating that Google Cloud is “compute constrained” in the near term. Hyperscaler capex commitments continue to be revised upward rather than downward, with the AWS and Google Cloud backlogs now sitting at $364B and $460B respectively. The combined ARR of OpenAI and Anthropic continues to compound at rates no previous software category has approached. None of these are the signatures of a frenzy approaching its peak — they are the signatures of a frenzy still gathering pace.

That tells me the frenzy phase still has some time to run. The crisis, when it eventually comes, will most likely look like a combination of valuation correction, geopolitical disruption, and political response to labour displacement. It will not be the end of the technology. It will be the gateway to the deployment phase.

6. What the Cycle Tells Us — Lessons From Past Installations

Knowing where we sit in the cycle is one thing. Knowing what the cycle has done at this point in every previous iteration is another, and arguably more useful. Perez's framework gives us five comparable cases — 1771, 1829, 1875, 1908, 1971 — and despite the obvious differences in technology, geography, and institutional context, a handful of structural patterns recur across all five with remarkable consistency. Five lessons worth working through specifically below.

The companies that lead installation are rarely the companies that lead deployment. The railway mania of the 1840s ended with most of the speculative railway companies bankrupt. The eventual railway industry leaders — the consolidated regional networks of the late nineteenth century — emerged from the wreckage of the bubble, not from its peak. Almost none of the household-name companies of the dot-com bubble (Pets.com, Webvan, Worldcom, Lucent, Sun Microsystems) led the deployment phase that followed. The actual deployment leaders — Amazon, Google, Facebook, the cloud hyperscalers — were either smaller during the bubble or did not exist yet.

The implication for the current cycle is that the public-market darlings of 2024–2026 may not be the durable winners of 2030–2045. The frenzy-phase sellers of the shortage are riding margin expansion that almost certainly compresses when supply catches up. The frontier model labs are extraordinarily valuable today, but the historical pattern suggests their commercial dominance will look very different on the other side of the turning point. The companies that actually lead the deployment phase are most likely to be the ones building the application layer that productively monetises the infrastructure being installed today.

The turning-point crisis is usually triggered by something the consensus didn’t anticipate. The 1929 crash was the conclusion of a long-running speculation, but the specific timing was driven by Federal Reserve tightening. The 2000 crash was triggered by interest-rate adjustments, accounting scandals, and supply-side saturation. The 1846 railway crash was triggered by collapsing demand for the bonds funding the speculative railways. In each case, the crisis came from a direction the market was not fully pricing. I have no idea what triggers the AI turning-point crisis, but it almost certainly will not be the obvious thing.

Deployment lasts longer than installation, and it pays better. The frenzy-phase returns are spectacular but compressed; the deployment-phase returns are slower but considerably more durable. The post-1929 deployment phase delivered the longest period of equity outperformance in modern American history — the Dow rose roughly tenfold in real terms between 1949 and 1966, against a backdrop of broadly rising real wages and falling inequality. The post-2000 deployment phase has delivered Amazon, Google, Microsoft, Apple — companies whose value creation since 2010 has dwarfed anything done by the dot-com winners. The pattern is consistent across cycles: the frenzy compresses extraordinary returns into a short window, the turning-point crisis wipes out the speculative cohort, and the deployment phase delivers genuine compounding to whoever has held correctly through it.

Institutional adaptation is slow but essential — and it determines the shape of the deployment phase. Perez argues that institutions are built for the previous paradigm and create active friction against the new one. This is the institutional inertia point. The 1930s saw Glass-Steagall, the New Deal, and Bretton Woods. The 2008–2015 period saw Dodd-Frank, the European Stability Mechanism, central bank reform. Each round of institutional reform reshaped what was possible during the deployment phase that followed. The post-AI-crisis period will require its own institutional adaptation — almost certainly involving labour-market policy, regulation of agentic systems, and adjustments to the international order around AI capability access. That adjustment will be politically difficult. It will also define the character of the deployment phase that follows.

Surges overlap. The maturity phase of one surge is also the gestation phase of the next. The cheap input of the next paradigm is being developed during the deployment phase of the current one. AI as a technology has been gestating since the 1950s, but the cheap-intelligence economics that make it the core of a new surge only became viable during the deployment of the fifth surge — through Moore’s Law, cloud computing, and the data accumulation that came with the internet. The ICT surge is what made the AI surge economically possible. The two are stacked, not separate.

Taken together, these five patterns describe the structural logic of the cycle, not its surface behaviour. The technologies change. The geographies change. The institutional context changes. But the underlying dynamics — financial capital, institutional inertia, diffusion, productive deployment — recur with enough consistency that they constitute the closest thing to a historical base rate the framework offers. The AI cycle will have its own specifics but will likely follow a similar structural pattern.

7. The Read From Here — Looking Ahead

From the framework, a small number of things follow that are worth holding onto. The framework is durable. The cycle has years to run. The cheap input of this surge is intelligence. The infrastructure is being built right now. The companies that lead the deployment phase will look different to the ones that lead the installation phase. The institutional choices made at and after the turning-point crisis will determine whether the deployment phase becomes a Golden Age or a stagnation regime. None of these are predictions. They are the structural reading of where we sit, anchored in 250 years of comparable cycles.

For me, that reading has three implications that have started to shape how I think about positioning. The first is patience. Deployment phases unfold over decades, not quarters. The companies and the institutional architecture that will define the AI surge are being built today, but their value won’t be visible until the turning-point crisis has resolved and the deployment phase has had time to play out. The second is selectivity. The historical record is clear that installation-phase winners and deployment-phase winners are usually not the same companies. The third is attention to the political economy. The Golden Age scenario is achievable but it is not the default — it requires deliberate institutional construction, and the conditions for that are less favourable now than they were after 1929 or 1945.

Even so, I am cautiously optimistic. The technology is real. The capital is committed. Institutional adaptation has reliably followed every previous turning-point crisis. The Golden Age scenario is harder to engineer than it was eighty years ago, but it is genuinely achievable — and the productivity gains being unlocked by cheap intelligence are large enough that the political pressure to distribute them broadly will eventually become unavoidable.

Where does this leave us? We are in the middle of the largest technological surge in modern economic history, the deployment phase has not yet started, and the choices that shape what that phase becomes are being made right now. The framework doesn’t tell you exactly what to do. But it does give you a mental model for reading the cycle you are actually in.

Great !

And I am writing an article exactly on this cycle, what are the chances . Completely agree with you. I picked up the first signal of such a cycle when the Hamas attack happened and then tracked events to come to a conclusion that this is a pattern, did not know about Kondrateiv or Carolina Perez till I searched for it