The 'Inflection Bubble': Understanding the AI Build-Out

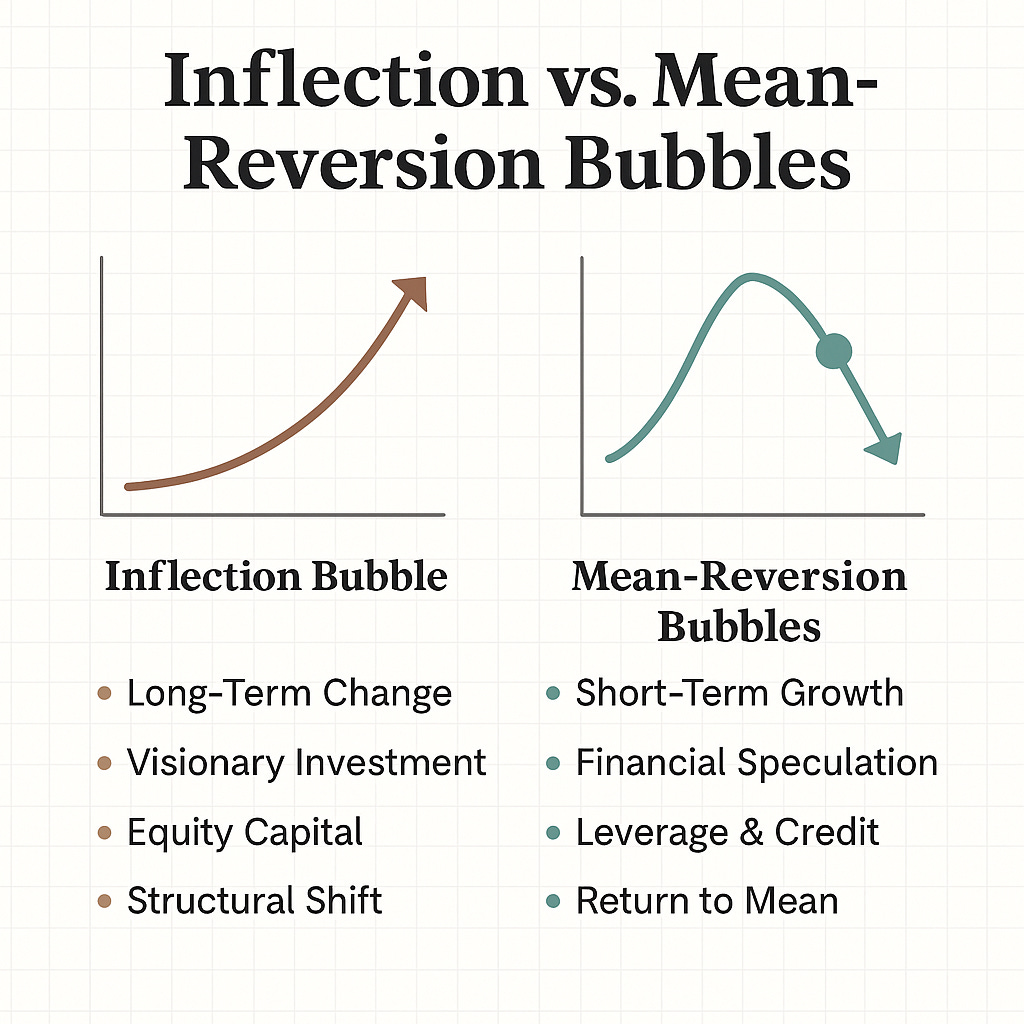

Inflection vs Mean Reversion Bubbles

At my recent investor event, I spoke about the idea of different types of market bubbles — a theme I’ve spent a number of years studying and thinking about. There’s a rich body of literature on the subject, but experience always brings me back to one truth: it’s impossible to know exactly where we are in a cycle. My goal here isn’t to call the top or bottom, but to offer a lens through which investors can make sense of today’s environment.

I hope this piece distils that thinking into a clear, logical framework. As Howard Marks famously put it, “no one knows” — and that much, at least, is certain.

1. Two Types of Bubbles: Mean-Reversion vs Inflection

Let’s begin with the foundation: what do I mean by bubble in this context, and how can we distinguish two very different kinds of bubbles that matter for investors, entrepreneurs and strategists.

In one version — call it the mean-reversion bubble — asset prices accelerate, often driven by credit, leverage, momentum and euphoria, only to revert back toward some historical norm. The archetype: housing in 2008, some sub-segments of the dot-com era, certain commodity cycles.

‘Mean-reversion bubbles occur when the price of an asset rises meaningfully above its historical average for no good reason and then returns to that average.’

Because the dynamic is essentially “we have x, we expect growth to keep going, so we bid up the multiple, then growth disappoints, and we’re forced back toward the mean.”

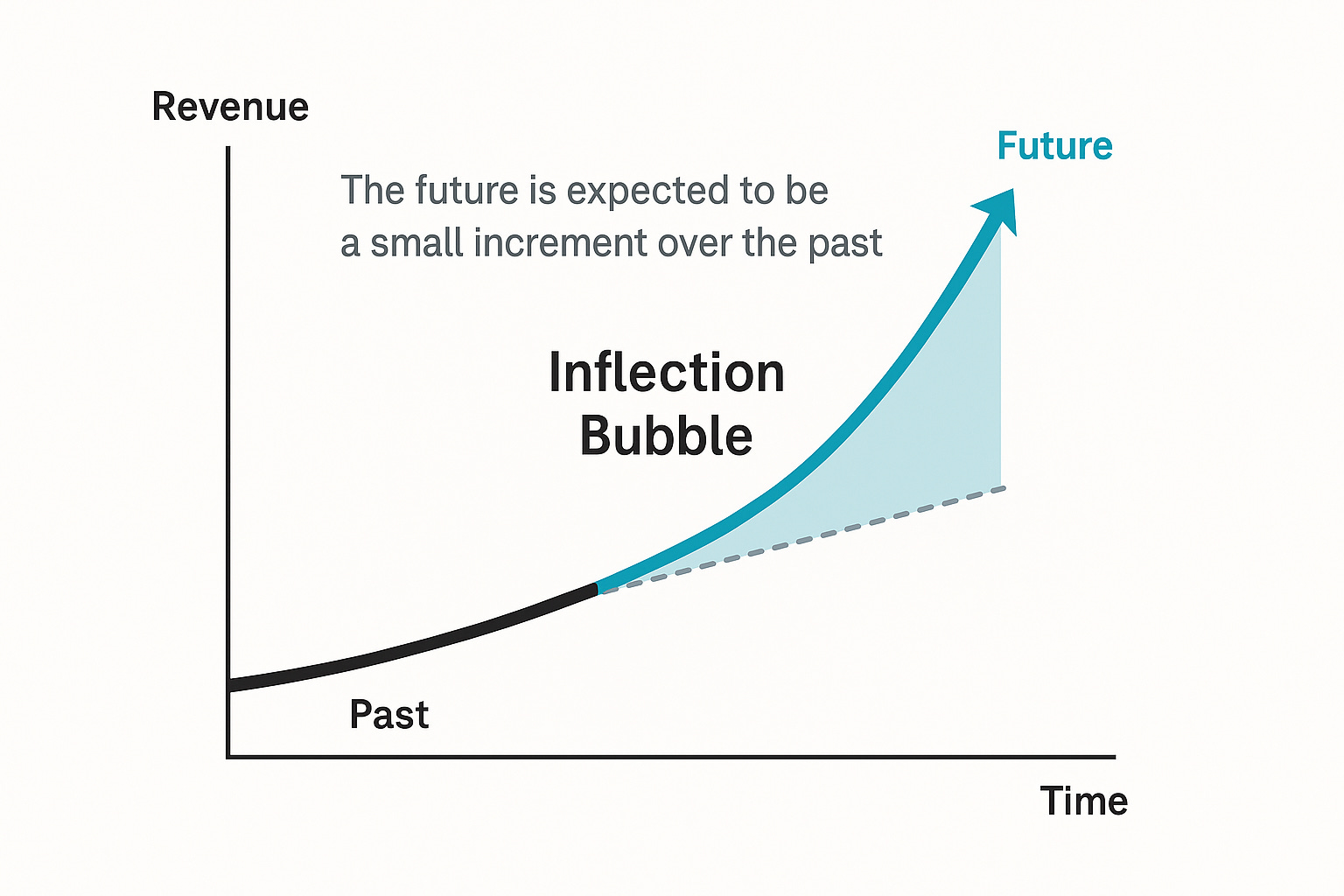

By contrast, the inflection bubble concept (as described by Byrne Hobart and Tobias Huber and popularised by others) is about belief in a fundamental shift — where the future is not a small increment over the past, but a new order of magnitude. Think of the telecom buildout in the late 90’s early 2000’s, and potentially the current AI capex buildout we’re experiencing today.

‘If a mean-reversion bubble is about the numbers after the decimal point, an inflection bubble is about orders of magnitude. In other words: companies, technologies or infrastructure are built on the assumption that “the future will meaningfully differ from the past.’

Crucially, the distinguishing features:

In mean-reversion bubbles, leverage, easy credit and financial speculation dominate; in inflection bubbles, equity capital and visionary investment often dominate.

The pay-off is not simply “we grew a bit faster” but “we changed the game” - this is the hallmark of an inflection related bubble.

And although an inflection bubble may still end in a shake-out, the infrastructure or capacity built often becomes the foundation of the next cycle.

As an example: the telecom / fibre / Internet build-out in the late 1990s and early 2000s has been characterised as an inflection bubble — many players lost money, but the fibre-optic networks became the backbone of the modern Internet. If you recognise whether you’re in a mean-reversion or an inflection bubble, you calibrate your strategy differently. If you think it’s mean-reversion, you’re cautious, you hedge for collapse. If you believe it’s inflection, you lean into long-term structural change, allocate to platform / infrastructure, and accept short-term noise.

2. Why The Current Cycle Looks Like an Inflection Bubble

With that framework laid, let’s turn to today, and make the case that we are in an inflection bubble — not just a frothy market, but a build-out of new infrastructure, new business models, and new scale.

Heavy capex by the hyperscalers

The recent reports on capital expenditure by large tech companies (“Magnificent 7” and other hyperscalers) suggest we are seeing an enduring buildout for AI infrastructure. For instance, one KPMG insight notes hyperscalers allocated over 50 % of their operating cash-flow to capex in 2023-24. Another piece shows that global data-centre and compute investment to 2030 may run to $5 – $7 trillion just for AI-capable infrastructure (McKinsey & Company).

This is not marginal. It’s not “we spend a little more this year” — it is a full-tilt build-out of compute, data-centres, power, cooling, chips, networking. We’re talking ground-up expansion of infrastructure.

No (or little) leverage, and the most profitable companies ever

One of the key features that make this bubble different from past ones is that much of the investment is being done by highly profitable, cash-rich companies, not by indebted borrowers or speculative levered players. That matters, because it reduces one of the main vectors of collapse in mean-reversion bubbles: forced deleveraging and margin calls.

By contrast, if the players funding the capex are cash machines (and many of the big tech players fit that description), then the dynamics shift. They can absorb mistakes, amortise over time, and are less exposed to “I must sell because I borrowed too much” pressures.

In other words: the investment is being done at scale by the winners — which suggests this is less about financial speculation and more about structural positioning.

Utilisation, supply bottlenecks & early innings

The infrastructure build-out is further justified by bottlenecks and low utilisation in the layer above (applications). For example: compute demand is spiking, yet supply of certain high-end chips, cooling, transmission / power remains constrained. McKinsey highlights the challenge of power, memory, and specialised hardware. Meanwhile, as evidenced in the recent MIT AI report enterprise adoption of AI applications outside the large tech players remains very low (c5 %), though intent to adopt is high.

In short: the green-field is still large. We’re not at 80 % saturation of “AI everywhere” in enterprises yet — probably closer to 5-10 % adoption of meaningful, production AI applications. That means the income and monetisation curves may still have a long tail of upside. Imagine if a portion of existing human labour budgets converge to software budgets, that alone creates a multi-multi trillion dollar market opportunity.

Why this could truly be an inflection and not just hype

Putting the above together:

You have vast capex being deployed.

You have new infrastructure whose purpose is to enable business models that did not exist before (or were constrained before).

The actors are large, cash-rich, and strategic rather than purely speculative.

The monetisation side (enterprise application layer) is still early.

The economics are not just “growth a bit faster” but “game-changing compute, game-changing AI, new workflows, new value-creation.”

This ticks the boxes of the inflection-bubble model rather than the mean-reversion model. I believe this is the build of the next cycle of innovation, and the “bubble” is not necessarily a warning sign but an invitation to position for structural change. To caveat, this could all change very quickly based on a few mis-steps/overestimation.

3. Inflection-Bubble Characteristics and the AI Buildout

Let’s take a step back and enumerate some of the key characteristics of inflection bubbles — both empirically and theoretically — and why they matter for strategy.

Key characteristics

Low leverage-to-equity: The investments are often equity funded. The risk of a cascade via debt is lower.

Large fixed-cost infrastructure: The early stage requires large build-outs to enable subsequent returns. Telecom fibre was the canonical example; today compute & data-centre is another.

Supply-side constraints: Because new infrastructure is being built, capacity matters; we don’t yet have “too much” supply everywhere.

Long lead-times: The time from infrastructure build to full monetisation is often long — this implies patience and optionality advantages.

New architectural shift: The value created is not simply more of the same, but qualitatively different. The Internet made networked computing ubiquitous; mobile changed the form factor; AI adds automation.

Coordination externalities: These bubbles often enable multiple players (hardware, software, networks, data) to coordinate implicitly via the frenzy of investment. That intensifies the ecosystem build-out.

Lower systemic risk: Because leverage is lower, the risk is less of a systemic crisis.

The AI build-out through this lens

Every one of those markers is visible today.

Global AI-capable data-centre investment could exceed $7 trillion by 2030 (McKinsey). In the first half of 2025, AI-related capex added more to U.S. GDP growth than consumer spending. Hyperscalers are committing billions of free cash flow to long-term GPU and accelerator supply contracts, while energy and cooling have become critical constraints. This isn’t a cloud upgrade — it’s an architectural reset of global compute.

Chip supply chains are stretched, HBM memory is scarce, and power grids are near saturation in key data-centre regions. S&P Global highlights energy access as the number-one bottleneck.

Meanwhile, less than 10 % of enterprises have fully deployed AI in production. The infrastructure is racing ahead of adoption — exactly what you’d expect in an inflection phase. The hyperscalers are building for an economy that doesn’t exist yet, but almost certainly will.

Because the primary funders — Microsoft, Meta, Amazon, Google — are cash-rich and unlevered, the risk profile is entirely different from past bubbles. The system can absorb missteps without triggering contagion.

We’re still early: adoption is 5–10 %, utilisation is 100 %, and the physical constraints are real. Investors tend to overestimate what can be achieved in the short term, but massively underestimate the long term.

In other words, the AI build-out is behaving exactly as an inflection bubble should: capital-intensive, equity-funded, capacity-constrained, and structurally self-reinforcing.

4. The Risk Curve and the Architecture of Value

No build-out this large comes without risk. Even genuine inflection bubbles carry structural uncertainties — they just tend to bend, not break.

Where the risks lie

Monetisation risk. Infrastructure alone doesn’t guarantee returns. Compute costs, GPU depreciation, and the uncertain economics of inference could compress margins before application-layer value catches up.

Misallocation risk. The history of telecom and energy build-outs reminds us that not all capex compounds. Building in the wrong region, architecture, or cooling regime could strand billions in assets.

Timing risk. The structural thesis may be right, but the payoff slow. The gap between infrastructure readiness and mass adoption is measured in years, not quarters. Early capital often looks premature before it looks prescient. The existing circular revenue agreements between hyperscalers and model providers could further exacerbate this this.

Energy constraint. AI data-centres could require an additional 150–200 GW of generation capacity this decade (McKinsey). If grid expansion lags, the limiting factor won’t be capital — it’ll be electrons. This is where China currently has a major advantage vs ROW.

How value will ultimately accrue

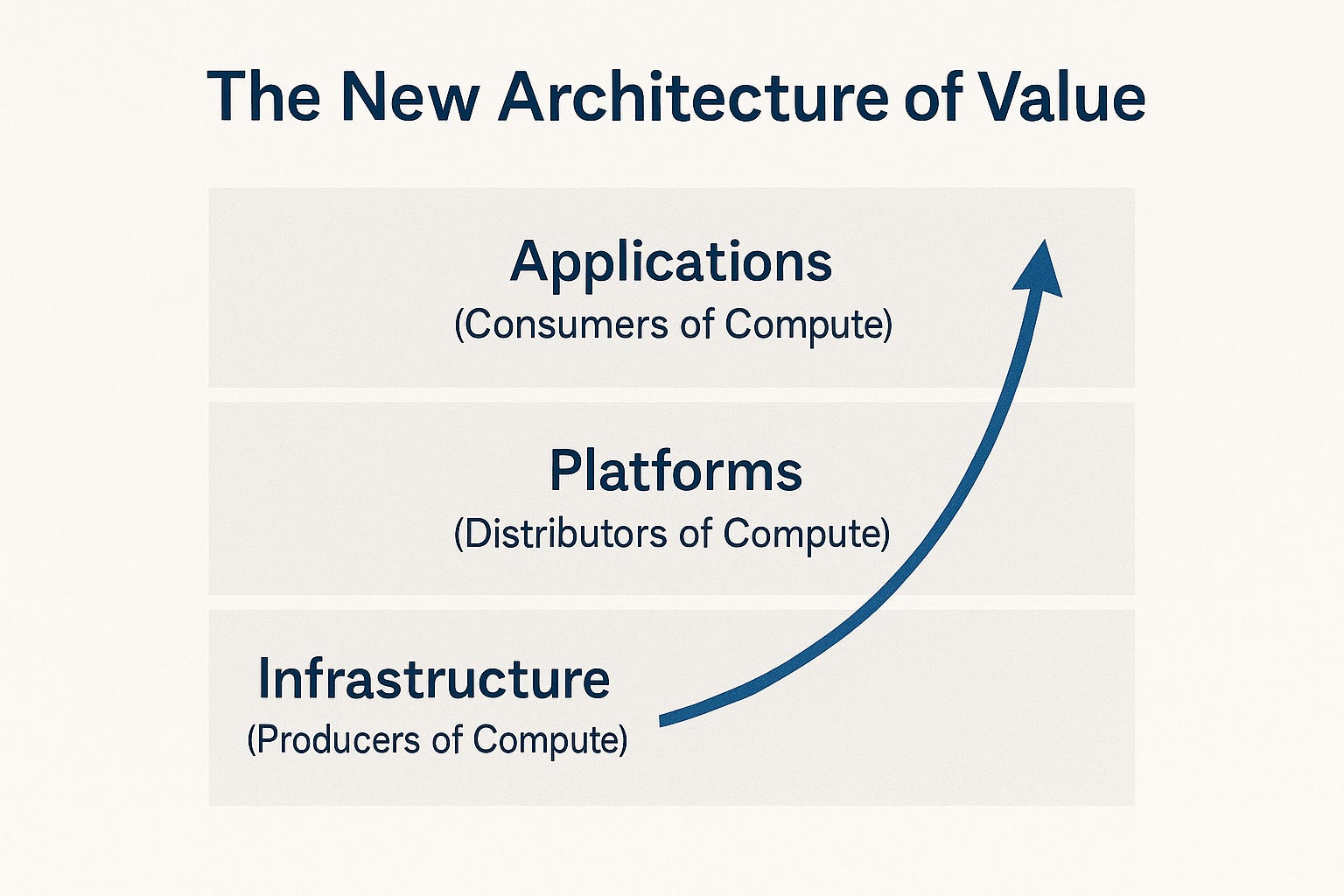

Every major technological inflection reshapes the profit map. Railways, fibre, and cloud all began with infrastructure euphoria, but the lasting wealth creation occurred higher up the stack — in the businesses that used the new infrastructure most efficiently.

AI is following the same pattern:

Infrastructure (Producers of Compute and Model Providers): Nvidia, TSMC, OpenAI, Anthropic and energy suppliers — the shovel-sellers of this era. They’ll enjoy extraordinary returns while scarcity persists but will normalise as capacity catches up.

Platforms (Distributors of Compute): AWS, Azure, and Google Cloud — the utilities of the AI age, durable but increasingly regulated and margin-bound once the build phase peaks.

Applications (Consumers of Compute): this is where the next decade’s venture alpha will be created. The companies that can convert $1 of compute into $10 + of enterprise value — the highest “Compute ROI Ratio” — will define the next cycle.

The irony is that the platforms are subsidising their future customers: they’re financing the infrastructure that tomorrow’s AI-native software companies will monetise. The hyperscalers are laying the tracks, but it’s the next generation of AI native/AI enabled software companies that will likely be the major beneficiaries (as I covered in my previous article - producers vs consumers of compute).

5. The shape of what comes next

If this truly is an inflection bubble, it won’t burst — it will decompress.

Valuations will reset, excesses will fade, but the infrastructure will remain and productivity will compound on top of it.

This cycle is unique in three ways:

Cash-funded, not credit-funded. The Mag 7 are self-financing a multi-trillion build-out with record free cashflow. No systemic leverage to unwind.

Productive, not extractive. Every GPU installed expands capability; the waste is functional, building the substrate of the next economy.

Constrained by physics, not liquidity. Energy, grid capacity, and chip yield — not capital markets — are the bottlenecks.

From an investor’s lens, this feels less like 1999 and more like 2003: the unglamorous but crucial phase when foundations were laid and the enduring winners quietly scaled. The hype will fade; the adoption curve has barely begun. Enterprise AI penetration sits around 5 %. The next decade will be about monetising the rails being built now.

If history rhymes, the infrastructure being built today will underpin the next trillion-dollar generation of technology companies.