Deconstructing the ‘Software-mageddon’: Why Software Isn't Dead

From Systems of Record to Systems of Action

Given the amount of noise in the market this week, it felt like the right moment to share my thinking on what’s being framed as a drought across software. I’ve also had a steady stream of messages from my network asking for my view, which usually tells me the narrative has run well ahead of the underlying reality.

There’s no shortage of commentary suggesting that enterprise software is on the brink of collapse—that AI will unwind two decades of value creation almost overnight. Most of it is confident, much of it is simplistic, and very little of it engages with how high quality software actually functions inside large organisations.

In this piece, I’ve tried to step back from the headlines and lay out a clearer framework for thinking about what’s really changing, what isn’t, and where some of the smartest operators and business leaders are focusing their attention. The aim isn’t to make a market call or argue that this is some obvious buying opportunity—that’s neither the point nor something I pretend to have an edge on—but rather to offer a way of reasoning about the moment we’re in, so you can form your own view on the current state of software.

1. The Panic of February 2026: Deconstructing the ‘Software-mageddon’

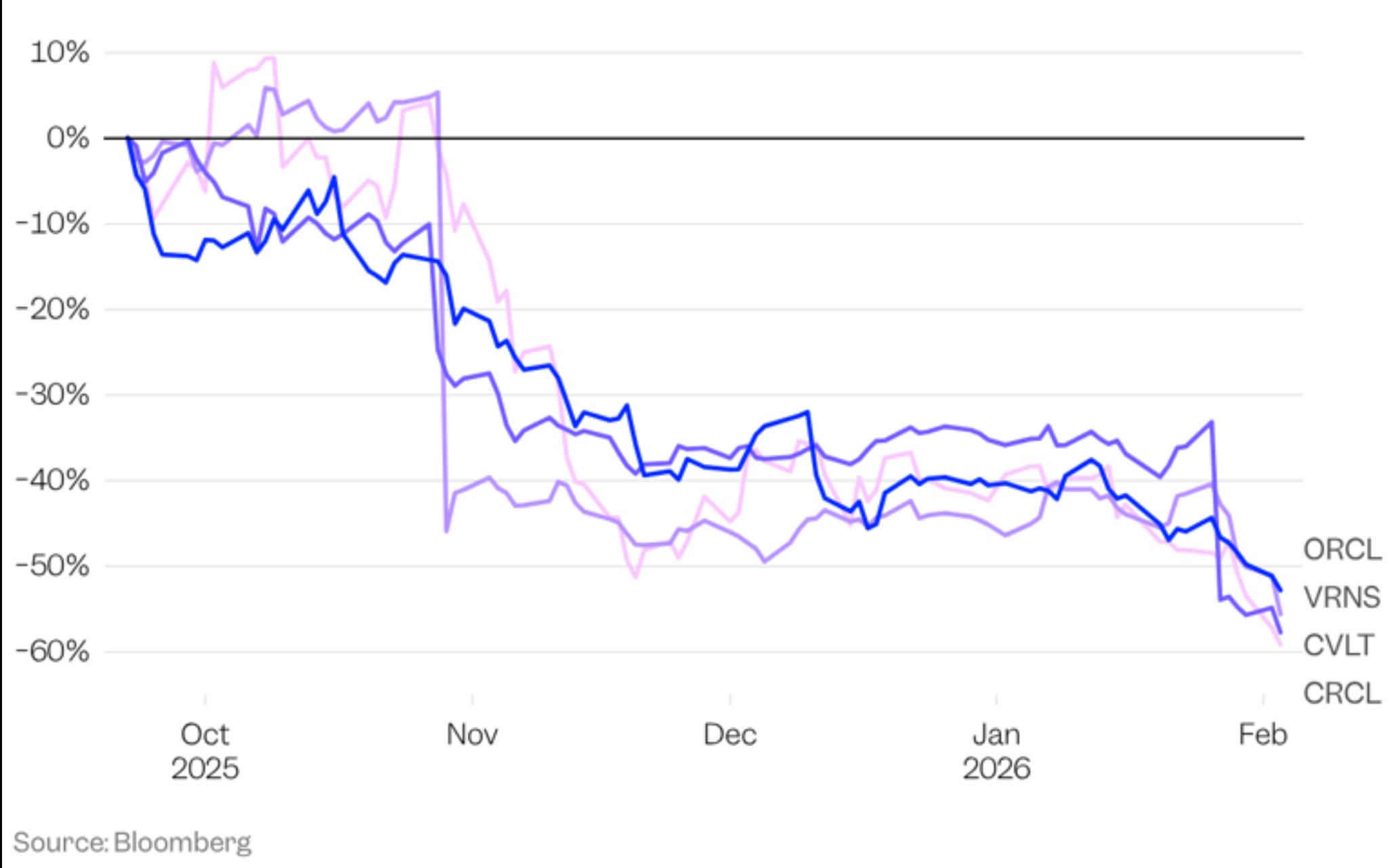

The technological landscape of February 2026 has been defined by a profound and visceral reassessment of the enterprise software sector. What began as a series of incremental advancements in autonomous agent capabilities culminated in a week of unprecedented market volatility, often referred to in financial circles as “Software-mageddon”. During this period, a sharp divergence emerged between the skyrocketing valuations of artificial intelligence (AI) infrastructure providers and the precipitous decline of established Software-as-a-Service (SaaS) incumbents. The prevailing market narrative shifted from “AI as an enabler” to “AI as an extinguisher,” predicated on the fear that autonomous agents will eventually bypass traditional software interfaces entirely, making the very concept of a software “application” redundant.

However, a rigorous analysis of the structural moats—distribution, data gravity, regulatory compliance, and mission-critical integration—suggests that the obituary for the software industry is premature. While the “per-seat” productivity model is undoubtedly under siege, the high-quality, deeply integrated software companies of the cloud era are not being replaced; they are being fundamentally re-architected into ‘AI enablers’. This article examines the mechanics of this transformation, arguing that the true winners of the AI era will be those durable incumbents that successfully overlay an agentic workflow layer across their massive existing data repositories.

The February 2026 Software Crash

The first week of February 2026 serves as a case study in the power of narrative-driven market corrections. Following the launch of Anthropic’s “Claude Cowork,” which demonstrated a remarkable ability to automate complex back-office workflows and professional services, investors began to systematically de-risk their portfolios of traditional software exposure. The result was a staggering $1 trillion loss in market value for U.S. software and services companies in just seven sessions. The Dow Jones software index plummeted 3.48%, and the computer services index tumbled 7.70% in a single day, as fears intensified that generative AI would cannibalize the high-margin subscription models that have underpinned Silicon Valley for two decades.

This sell-off was fueled by comments from prominent figures and research analysts who posited that “legacy software that’s old and clunky is a ripe target for AI”. The market’s skepticism was compounded by the fact that many software firms, despite racing to implement AI features, had yet to see these efforts bear significant fruit in terms of revenue growth or margin expansion. Evidence surfaced that disruptive AI tools were already pressuring the pricing power of former market leaders; for instance, Docusign’s Return on Equity (ROE) plummeted from 169% to 39%, while Atlassian’s projected earnings growth for 2026 slowed significantly as the market braced for AI-driven disruption.

The panic was not localized to the United States. In India, the $283 billion IT services industry—a cornerstone of the global software ecosystem—saw its worst session in nearly six years. Large exporters like Tech Mahindra, TCS, and Infosys, which rely on application services for 40% to 70% of their revenue, faced an existential threat as AI-driven automation from companies like Anthropic and Palantir promised to compress project timelines and erode the billable-hour model. Analysts estimated that between 9% and 12% of the industry’s revenue could be eliminated over the next four years as AI tools allow businesses to do more with significantly fewer staff.

The Redundancy Thesis: Why Markets Fear the AI Agent

At the heart of the “Death of SaaS” narrative is the realisation that traditional software applications were essentially tools that required human operators to function. For twenty years, companies like Salesforce and Slack sold “Software-as-a-Service,” but in practice, they provided digital workbenches that users had to learn and operate. Microsoft CEO Satya Nadella’s proclamation that “applications as we know them are going away in favour of agents” catalysed the fear that the “application layer” is an unnecessary middleman between human intent and the underlying data.

This evolution is often described as the shift from SaaS to “Service-as-Software” (SaS), where the customer no longer pays for access to a tool but for the completion of a specific outcome. If an AI agent can research a legal contract, draft a response, and file it autonomously, the need for a “contract management software” seat diminishes. This outcome-based model directly threatens the “per-seat” pricing that has allowed SaaS companies to scale alongside the growth of their customers’ headcounts.

The “Illogical” Fallacy: Leadership’s Defence of Software

As the markets spiralled, the world’s most influential tech leaders stepped in to challenge the redundancy narrative. Nvidia CEO Jensen Huang, speaking at a Cisco conference in San Francisco, described the fear that AI would replace software as “the most illogical thing in the world.” Huang argued that software is the core tool, and AI is simply a new user of that tool.

“If you were a human or robot, would you use tools or reinvent tools? The answer, obviously, is to use tools,” Huang noted, emphasising that the most remarkable advances in AI are about “tool use” because those tools—like CRMs and ERPs—are explicitly designed to handle business logic. For Huang, AI doesn’t render software redundant; it makes it more valuable by allowing “digital labor” to operate it 24/7.

Video Clip: Jensen Huang - Software

Salesforce CEO Marc Benioff echoed this sentiment, flatly stating that “SaaS is not dead.” Benioff has pivoted Salesforce toward “Agentforce,” a platform that treats AI agents as a new workforce rather than a replacement for the software itself. He noted that the business logic is moving into these agents, but they still require a “System of Record” to prevent them from “hallucinating” or inventing data. Microsoft CEO Satya Nadella also described AI as an “enabling tool,” suggesting that while the interface might shift toward agents, the underlying “token factories” and data infrastructure remain the bedrock of the economy.

2. The Data Advantage: From Systems of Record to Systems of Action

The “Death of SaaS” argument consistently underestimates one thing: just how hard enterprise data is to manage, govern, and operationalise at scale.

For an AI agent to be genuinely useful inside an organisation, it needs context. Not abstract intelligence, but grounded, situational awareness. It needs to know which customer is complaining, what their historical billing status looks like, how similar cases were resolved in the past, what contractual constraints apply, and where decision rights sit. None of that context lives inside a generic large language model. It lives inside the databases, schemas, and workflows of the very software platforms currently being written off by the market.

This is where high-quality incumbents retain a decisive edge. Over decades, they’ve accumulated what is best described as data gravity: the tendency for data, applications, permissions, and processes to cluster together over time. Data attracts logic. Logic attracts workflows. Workflows attract users. And eventually, the system becomes unavoidable. What’s changing in the AI era is not the importance of these systems, but their role.

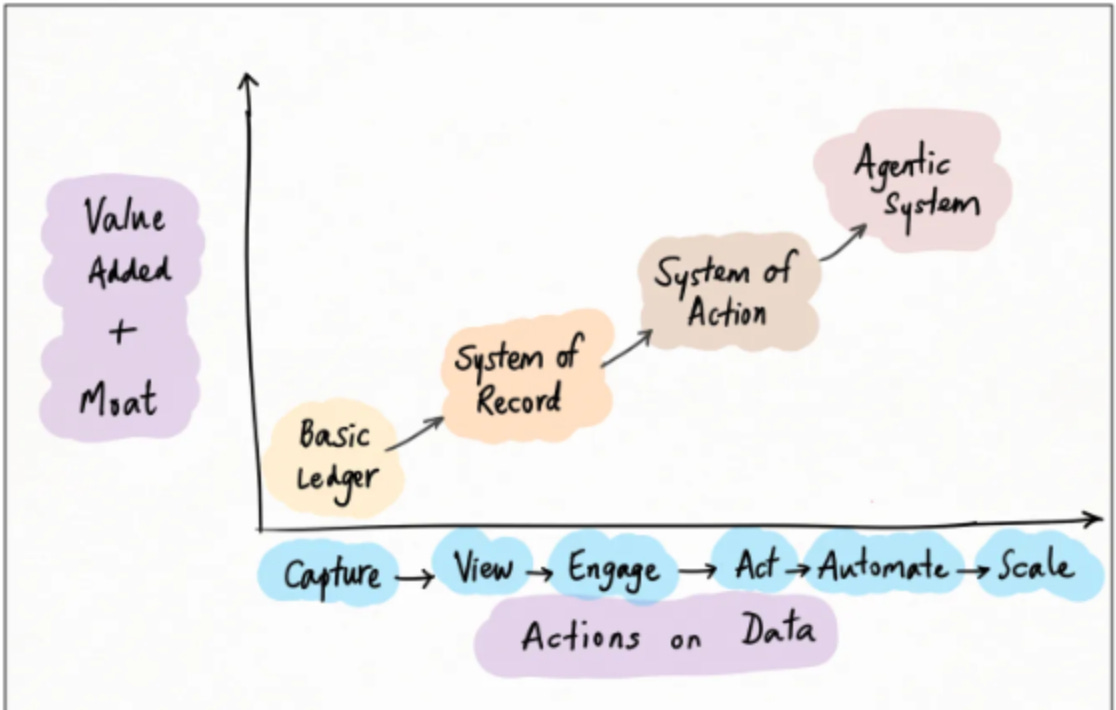

Historically, enterprise platforms were systems of record. Their job was to store information accurately, enforce rules, and provide an auditable source of truth. CRMs recorded customer interactions. ERPs tracked inventory, finance, and supply chains. Observability tools logged what happened after the fact. They were passive repositories—critical, but reactive. AI enables a shift from systems of record to systems of action.

In a system of action, the software doesn’t just store data; it actively reasons over it, proposes decisions, and increasingly executes workflows—under governance. The system moves from being a database you query, to an operational brain you direct. This transition is only possible because the underlying data is structured, permissioned, and trusted.

Crucially, incumbents are not “bolting on” a chatbot and hoping for the best. They are layering agentic workflows directly on top of their proprietary data estates. That allows them to offer a unified, governed context that AI-native startups simply cannot replicate without years of painful integration work. An AI agent operating inside a CRM or ERP doesn’t need to guess. It can check. It can validate. It can reconcile intent with policy. That distinction—between suggestion and sanctioned action—is everything in the enterprise.

The Mechanics of the Agentic Workflow Layer

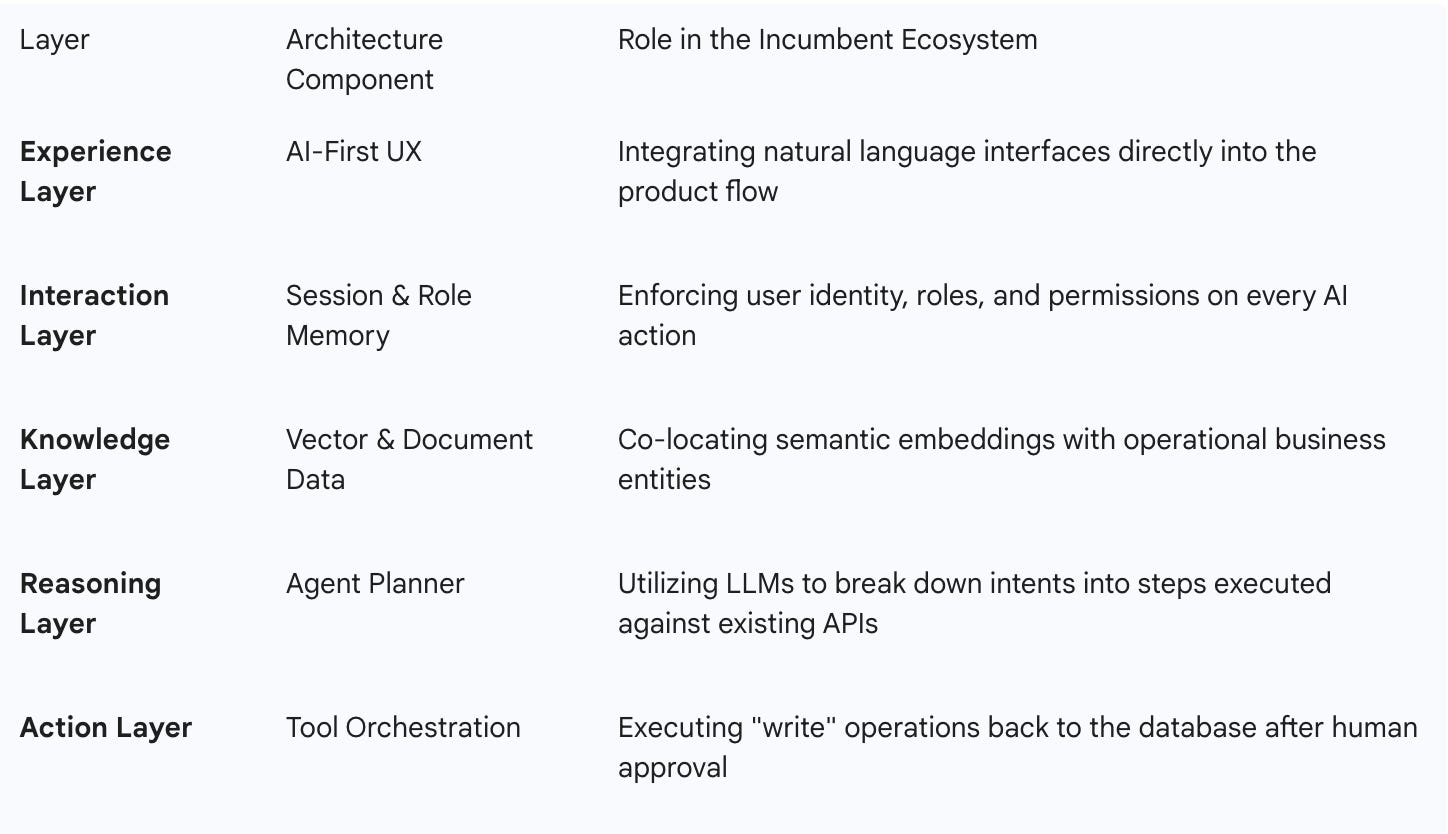

Modern agentic architecture in established SaaS is built on a “converged datastore” model. Companies like MongoDB and SAP are evolving their architectures to support four primary layers that enable truly agentic AI systems while maintaining the integrity of the “system of record”.

This converged architecture allows AI agents to inhibit the data, maintaining persistent memories across interactions. For instance, MongoDB Atlas Vector Search enables meaning-based retrieval across billions of embeddings that are stored alongside the actual business objects. This co-location eliminates the “synchronization tax”—the time and cost required to sync data between a standalone vector database and an operational database—which is a major bottleneck for AI-native startups.

Furthermore, the “Truth Layer” remains the most significant moat. Enterprises pay a premium for software because it provides a deterministic environment where rules are enforced and data is auditable. If an AI agent autonomously suggests a price discount, it must check the company’s financial policy, the customer’s contract, and the current inventory levels—all of which are managed by the ERP and CRM. SaaS platforms are inherently structured around these defined schemas and tightly bound logic; agentic workflows, while dynamic, depend on this structure to prevent hallucination.

3. Beyond Code: The Structural Moats of Distribution, Regulation, and Security

A common misconception among AI enthusiasts is that “code is the moat.” In reality, the defensibility of enterprise software has always been built on structural barriers that are difficult for even the most advanced AI to overcome: distribution networks, security certifications, and regulatory compliance. Code is just a way for faster, more efficient product evolution, which can be harnessed by both AI enabled and AI native companies.

The “Return on Hassle” and the Trust Moat

Fawad Qureshi of Snowflake has argued that the primary value of SaaS is the “Return on Hassle” (ROH). Enterprises outsource the “hassle” of managing data, security, and infrastructure to software providers so they can focus on their core business. AI agents, while powerful, often increase “hassle” in the early stages because they lack the deterministic controls of traditional software. Organisations in regulated industries like finance, healthcare, and manufacturing are hesitant to allow autonomous agents to make decisions without the seal of approval that comes with established software.

Regulatory events are the primary reason many software companies are “un-killable”. When a construction firm uses Procore, it isn’t just buying a tool; it is buying a legally-mandated audit trail for its projects. When a bank uses a specific platform for KYC compliance, the software becomes the “shield” protecting the company from existential legal and financial risks. Switching away from a verified system of compliance to a new AI-native startup introduces a level of corporate liability that no board of directors would approve just to save on a license fee.

Security Certifications as Barriers to Entry

The complexity of enterprise-grade security cannot be overstated. High-quality software companies have spent years and millions of dollars achieving certifications that are now the “table stakes” for doing business with the Global 2000.

SOC 2 Type II - Requires rigorous, long-term evidence of data security and privacy controls

ISO 27001 / 42001 - Standardizes information security and responsible AI development management

HIPAA - Mandatory for any software handling protected health information (PHI)

EU AI Act - Enforces strict risk-based guidelines for AI providers in the European market

GDPR / CCPA - Complex data “right to be forgotten” rules that are difficult to implement in LLMs

For an AI-native startup to compete with a company like SAP or Salesforce, it must not only match the product’s capabilities but also replicate the entire compliance and security infrastructure. Established vendors benefit from “mature integration ecosystems” and robust, standardised API connections that are hardened by years of production use. They are “compliance-by-design,” whereas agentic AI systems are inherently decentralised and adaptive, making them harder to audit and secure. Especially when AI system is fully autonomous vs augmented.

Distribution and the Sales Cycle Moat

Distribution is where most scalable AI ideas struggle. While an AI startup might have a superior algorithm, it lacks the “Master Service Agreements” and the deeply embedded sales relationships that incumbents enjoy. The enterprise sales cycle is notoriously long, often taking 120 to 360 days for deals over $100,000. Incumbents have the advantage of “cross-selling” AI capabilities to an existing customer base that has already cleared the legal and procurement hurdles. A way to increase ACV and drive Net Revenue Retention.

For example, Shopify’s “Universal Commerce Protocol” (UCP) allows any merchant on its platform to immediately become “agentic-ready,” surfacing their products on ChatGPT and Gemini without any new integration work. A startup trying to build a new agentic commerce platform would have to convince millions of merchants to individually integrate their data—an integration bottleneck that Shopify has already solved.

4. Case Studies: High-Quality Incumbents as AI Enablers

The transition from “software as a tool” to “software as a conductor” is already visible in the strategies of market leaders. These companies are proving that they can thrive by becoming the infrastructure that AI agents use to perform work.

Salesforce: The Operating System for Enterprise AI

Despite the “Death of SaaS” narrative hitting Salesforce particularly hard in the markets, the company’s internal data tells a different story. Salesforce has positioned its “Agentforce” as a “consumption flywheel” that is spinning faster than anticipated. By Q3 2025, the number of Agentforce customers in production had increased 70% quarter-over-quarter, and the product reached an ARR of $540 million—a 330% increase year-over-year.

Salesforce’s moat is its ability to provide a “360-degree view” of the customer that is “securely hosting information that is accessible by all relevant parties”. Even if an AI agent automates a task, the enterprise still needs a centralised CRM as a “source of truth” to ensure that agents don’t invent data. Salesforce is even willing to lose money on short-term agent licenses to ensure that it remains the trusted operating system for the next decade of enterprise work.

SAP: Moving from Firefighting to Orchestration

SAP is leveraging AI to move the ERP from a “system of record” to a “system of orchestration”. In 2026, SAP’s strategy is built around “Intent-driven ERP,” where users express high-level goals—like “optimise the supply chain for a sudden demand spike in Asia”—and AI agents plan and execute the steps across planning, logistics, and procurement.

Manufacturers using SAP’s embedded AI have reported:

40% reduction in equipment downtime through predictive maintenance.

25% improvement in production efficiency through automated scheduling.

15% cost reduction across global operations.

SAP’s approach utilises agentic AI to drive quicker, more cost-effective migrations to S/4HANA, reducing technical debt and accelerating the time-to-value for digital transformations. For SAP, AI is not a competitor; it is the “conductor” that makes multiple silos and departments work in harmony. SAP is arguably the most deeply embedded software product ever created, architecting the ‘modular’ software approach which drives incredibly high switching costs and makes it almost impossible for customers to leave.

Datadog: Observability in the Distributed AI Age

As AI applications become more complex, the need for “observability” grows. Datadog has expanded its platform to provide visibility at every layer of the AI stack, from GPU monitoring to “LLM Experiments”. Traditional monitoring tools fall short because they assume software is deterministic; AI systems, however, degrade gradually through drift or bias.

Datadog’s “Watchdog AI” uses unsupervised machine learning to flag unusual behaviour across cloud and Kubernetes environments without needing explicit baselines. By ingesting billions of data points daily, Datadog can correlate a subtle backend latency spike with a specific AI model’s performance—a level of analysis that standalone AI tools cannot match. This integration makes Datadog an essential partner for any organisation trying to run AI at scale reliably and securely.

Shopify and the Renaissance of Agentic Commerce

Shopify is pushing“agentic commerce,” where AI systems actively manage workflows and distribute products into third-party ecosystems. Through the “Universal Commerce Protocol” (UCP), co-developed with Google, Shopify has created a shared language for AI agents to connect and transact with any merchant.

Key features of Shopify’s agentic shift include:

Agentic Storefronts: Allowing products to be discovered and purchased directly within AI conversations on ChatGPT or Perplexity.

Sidekick Pulse: A proactive agent that suggests product bundles based on real-time cart behavior and flags compliance gaps.

SimGym: An AI-powered “testing ground” that uses shopper agents to simulate human traffic and purchasing behaviour before a live rollout.

Shopify is no longer just a destination; it is a distributed set of data points that allows commerce to happen “everywhere people spend their time”. This distribution moat is nearly impossible for a new entrant to replicate. This is also an example of how network effects and scale economies create a significant competitive moat, both of which Shopify has in abundance.

MongoDB: The Cognitive Core for AI Memory

MongoDB has transformed its document database into the “cognitive core” for agentic AI. AI agents require memory to be effective, and MongoDB provides a unified platform for storing conversation history, agent profiles, and hierarchical states in a flexible format.

By co-locating vector search with operational data, MongoDB enables “Agentic RAG” (Retrieval-Augmented Generation), where an agent can dynamically choose the optimal retrieval tool—such as semantic search for intent and full-text search for exact keyword matches. This architecture supports thousands of concurrent agent sessions in a compliant way, making it the bedrock for mission-critical AI applications.

5. The Long-Term Outlook: Software as the Cognitive Core

The volatility we’re seeing today should be understood as a sales reckoning and a pricing model transition, not a terminal diagnosis for the software industry. What’s being challenged is not the relevance of enterprise software itself, but the assumption that value creation scales neatly with human headcount. That assumption held in a world where software existed primarily to augment people. It becomes fragile in a world where software increasingly acts.

High-quality, durable software companies will not only survive this transition—they are structurally positioned to benefit from it—but they will look meaningfully different on the other side. AI enablement does, without question, introduce real efficiency gains and cost compression. That will lead to displacement across certain organisational functions, particularly in roles optimised around coordination, process, and throughput rather than judgement or domain expertise. The “death of the B-player” in sales, support, and operations is real.

But this isn’t a story of wholesale replacement. It’s a story of recomposition. What replaces those roles is a higher-leverage human-plus-machine model, where fewer people oversee far more output. AI agents take on execution, while humans move up the value chain into supervision, exception handling, strategy, and ownership. Productivity doesn’t just increase—it becomes non-linear. One high-quality operator, properly augmented, can now do the work of ten.

This shift is uncomfortable because it breaks our intuition about how organisations scale. For decades, growth meant hiring. In the agentic era, growth increasingly means orchestration and AI enablement.

The Evolution of the Software Workforce and Pricing

This recomposition of work drives a parallel shift in how software is priced, sold, and justified. The move toward Service-as-Software changes the unit economics of the industry. Instead of paying for access to tools, enterprises pay for outcomes, throughput, and risk reduction.

In the near term, this puts pressure on traditional seat-based revenue models. Fewer seats are needed when agents do the work. But over the medium to long term, total software spend is unlikely to decline. In fact, it’s more likely to rise.

Why? Because the value delivered by “digital colleagues” is easier to measure, easier to attribute, and easier to justify at the board level. When an AI system demonstrably reduces downtime, accelerates cash collection, or improves conversion, it competes for budget against headcount, not against other software tools. That’s a far more defensible position.

What emerges is a clear organisational shift—from software as a productivity aid to software as an execution layer. Sales motions become more expert-led. User experiences move from dashboards to natural language. Value accrues to platforms that can safely translate intent into action. This transition also favours depth over breadth. Horizontal tools that optimise generic workflows face compression. Vertically embedded platforms—those deeply entangled with industry-specific data, regulation, and process—become more valuable, not less.

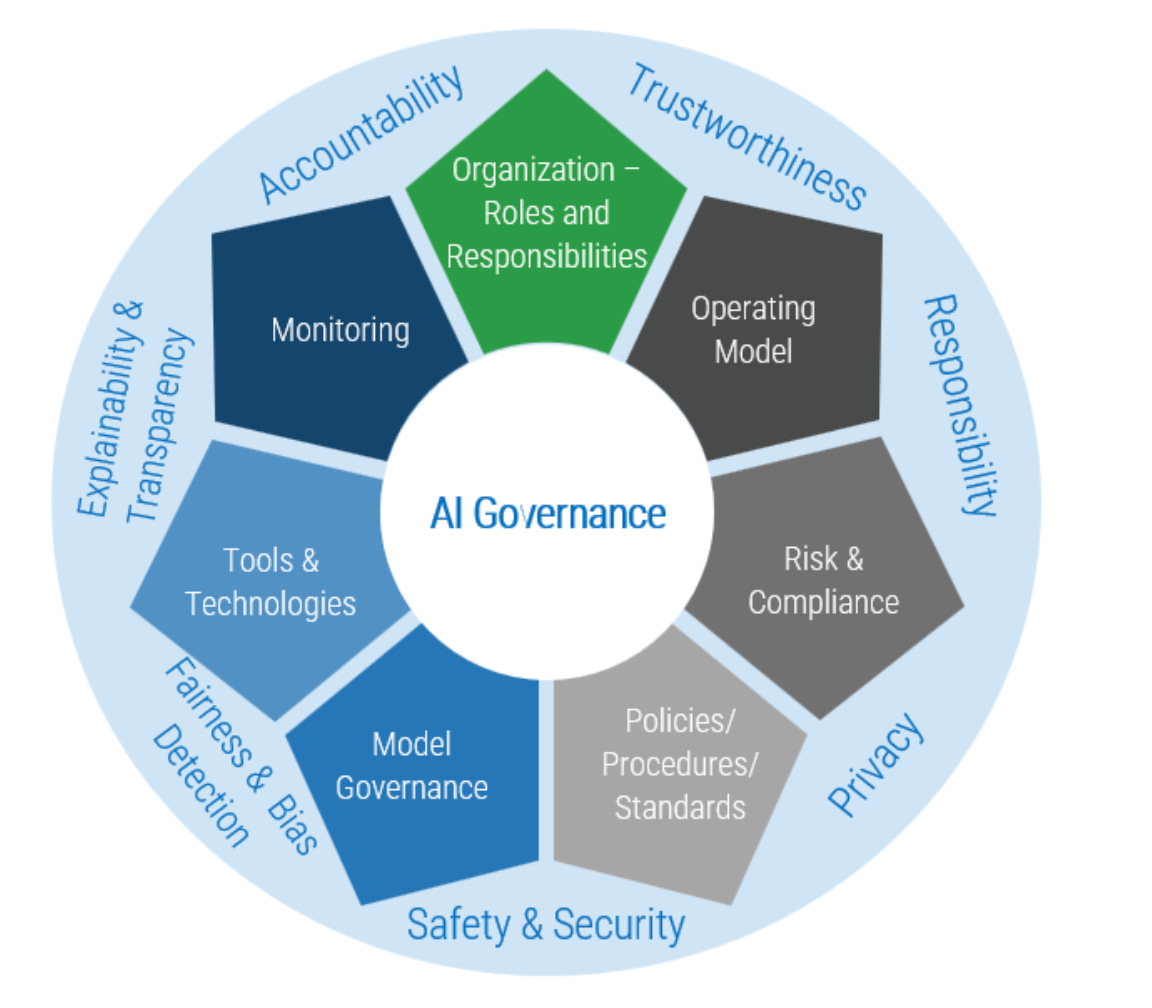

Sovereign AI and the Rise of Agentic Governance

Another defining theme is less about capability and more about control. Large enterprises are no longer asking, “What can AI do?” That question has largely been answered. The more important question is, “How do we govern it?”

As organisations deploy hundreds—or eventually thousands—of autonomous and semi-autonomous agents, the problem shifts from enablement to oversight. Who owns each agent? What data can it access? What actions is it authorised to take? How do you audit its decisions, monitor drift, and intervene when something goes wrong?

Enter Sovereign AI and Agentic Governance.

Enterprises will increasingly demand a virtual control tower—one that tracks every agent, enforces policy at the point of action, and provides a clear line of accountability. This governance layer is not an afterthought; it becomes core infrastructure. And once again, this plays directly into the strengths of existing software incumbents. They already manage identity, permissions, security, compliance, and audit trails. Extending those capabilities from humans to machines is an evolutionary step, not a reinvention.

In that sense, the future of enterprise software isn’t about fighting AI. It’s about becoming the cognitive core through which AI operates—setting boundaries, encoding institutional memory, and ensuring that autonomy scales without chaos. The market may still be debating whether software is being disrupted. Enterprises, quietly and pragmatically, are deciding who they trust to run their machines.

Conclusion

The fears that AI will completely replace software companies are based on a superficial understanding of how the enterprise operates. While AI agents can write code and automate tasks, they cannot replace the “systems of record” that provide the truth, the “distribution networks” that provide the customers, or the “compliance frameworks” that provide the trust.

The high-quality software companies that have seen their stocks freefall in early 2026—Salesforce, SAP, Shopify, Datadog, and MongoDB etc—are actually in a strong position to capitalise on the agentic era. They possess the “Data Gravity” and the “Institutional Memory” that AI needs to be useful. By becoming the “Conductors” of the AI-enabled enterprise, these firms are moving up the value chain, from providing tools to providing outcomes. The shift from system of record to system of action.

I believe the “Software-mageddon” of 2026 will eventually be viewed as a shakeout where the antiquated, clunky and old were indeed replaced, but the “mission-critical and deeply integrated” emerged stronger than ever. The future is most likely not “AI instead of Software,” but “Software as the Operating System for AI.” The durable incumbents are not dying; they are simply installing the cognitive core that will power the next twenty years of global commerce. The new architecture is built on data, trust, and distribution—and in those categories, high quality software still dominate.

Great note - the interesting question for me isn’t whether software rebounds, but which parts evolve into durable infrastructure versus which fade as AI compresses margins and rebuilds the stack. Interesting times